Is Social Security really that important for my retirement income?

Yes, it is.

On average, Social Security beneficiaries receive between $500,000-$1,000,000 in benefits.* This usually makes up around 40% of the average American’s retirement income. While the additional 60% is a large chunk to make up on your own, Social Security has some unique advantages.

Depending on how you file could add even more to your income stream. It is a permanent decision that affects the rest of your life, and your spouse’s life as well.

Your benefits have a built-in cost of living adjustment, meaning they increase automatically to match inflation. This helps your spending power stay the same the rest of your life.

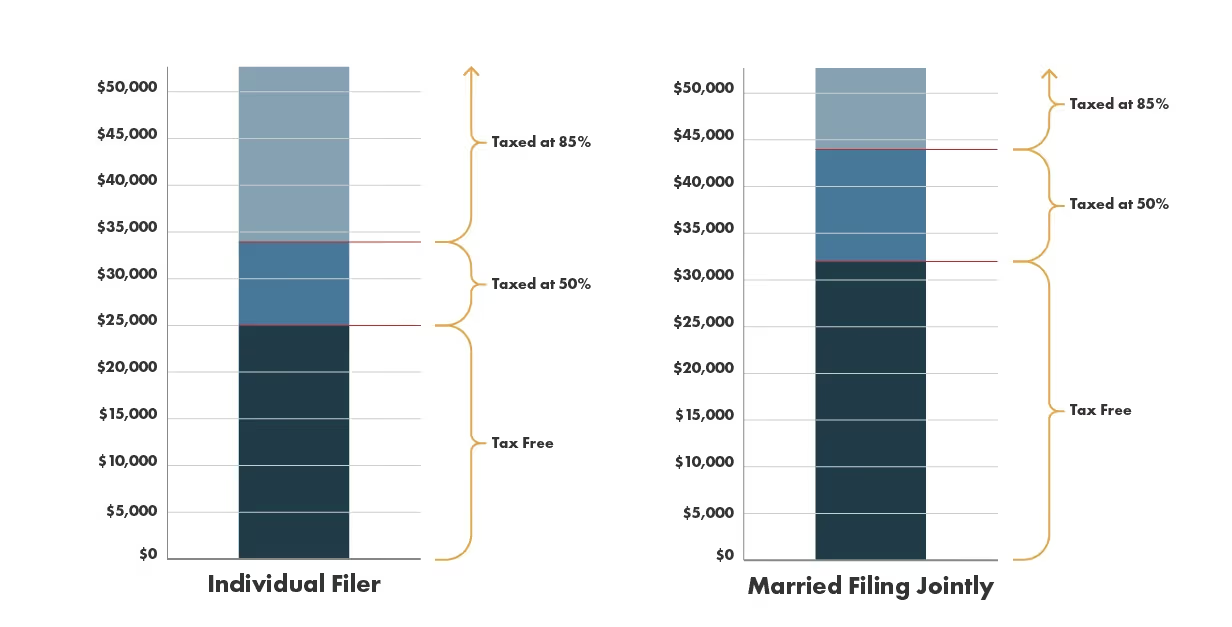

Also, your benefits are tax-advantaged. This means you won’t pay taxes on all of your Social Security income. At best, they could be tax-free, or at worst, you’ll pay taxes on a maximum of 85% of your benefits. How much you pay in taxes is determined by how much you make. Here are the details:

If you are an individual, you’ll pay no taxes on your benefits if your combined income is less than $25,000 and if you are married filing jointly, you’ll pay nothing under $32,000. Anything beyond that will be taxed at 50%. If your income gets higher than $34,000 for an individual, or $44,000 for married filing jointly, 85% of your benefits will be taxed. †

For example, say you are married filing jointly and have $20,000 of annual Social Security benefits. And after your other taxable income sources (withdrawing money from an IRA or 401k, or earned income from a job) your ‘combined income’ is $70,000. Since you fall into the higher benefits taxation, your taxes would look like this:

- 85% of your Social Security benefits is $17,000.

- In 2020, the Standard tax deduction is $27,400 if you are over the age 65 and you are married filing jointly.

- Remember your combined income is $70,000. Subtract $3,000 of Social Security benefits and $27,400 of your standard deduction from your combined income and you get $39,600. This is your total taxable income for the year.

So, you received $70,000 of total income and only had to pay taxes on $39,600.

The final way your benefits are unique is they are backed by the federal government. Few investments receive the strength and stability of the government supporting it. However, you might have heard the Social Security trust fund is set to run out in 2035. In our next post, you’ll find out why this shouldn’t worry you so much.

* “Social Security and Medicare Lifetime Benefits and Taxes: 2017 ….” 5 Jun. 2018, https://www.urban.org/research/publication/social-security-and-medicare-lifetime-benefits-and-taxes-2017-update. Accessed 30 Aug. 2019.

† “Benefits Planner | Income Taxes And Your Social Security Benefit ….” https://www.ssa.gov/planners/taxes.html. Accessed 30 Aug. 2019.

Continue Learning

Gain more Insights and empower your financial future with our articles and other resources.