When it comes to fees, how much is too much?

If you don’t know the specific fees in your investments you’re not alone. Through working with thousands nearing retirement, we’ve seen time and time again that most people don’t know the fees in their accounts, and many don’t realize they’re paying fees at all. That’s because, in the financial world, fees can be difficult to understand, or even worse, hidden. We don’t like that. Which is why we want to continue to provide insight and education on topics like this.

The truth is, you are paying fees and you could be paying a lot more than you think. And these fees could be eroding your retirement savings.

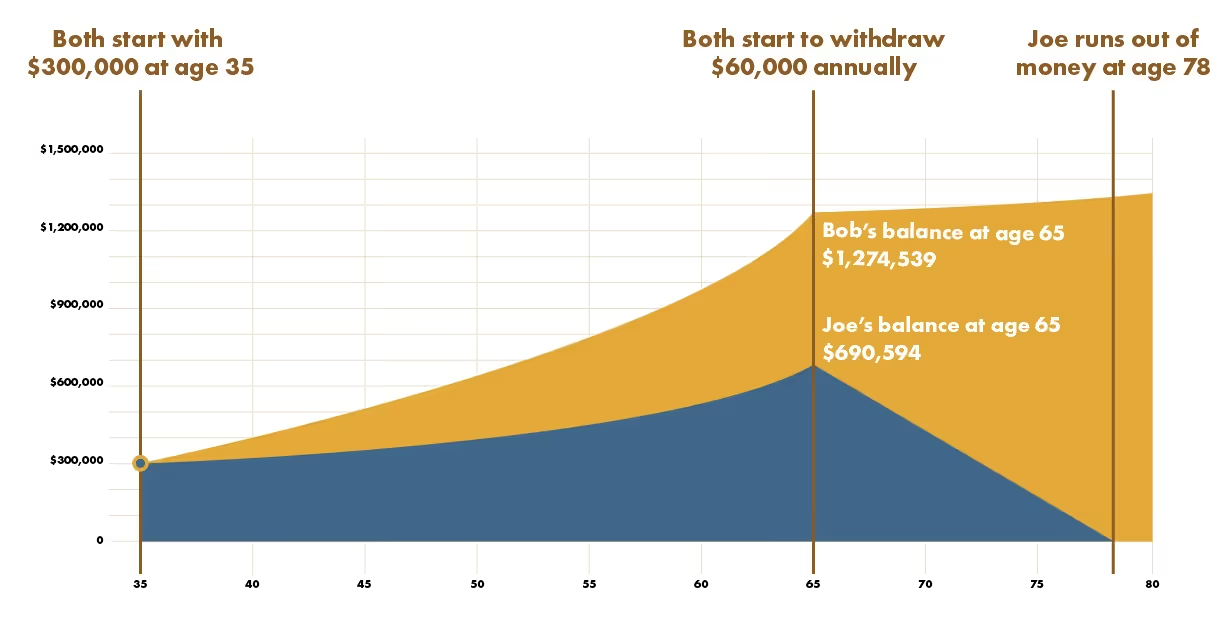

You might not think it’s a big deal. But here’s an example: Joe and Bob have IRA’s with a value of $300,000. Joe’s annual fees are 3% and Bob’s are 1%. Assuming they don’t add anything else to the account, and it grows an average of 6%, at the end of 30 years Joe’s account is worth $690,594 and Bob’s account is worth $1,274,539.

And when they retire at age 65 and withdraw a $60,000 annual income, Joe’s money runs out at age 78. Bob’s money never runs out. He gets to pass along an inheritance to his loved ones, a total of $1,322,837.

A difference of 2% fees can have a dramatic effect on your accounts. And there are many different types of fees to understand. So how do you know what fees you’re paying? Here’s a breakdown of the different fees so that you get an idea of what you could be paying.

There are two primary areas where you may have fees: investment fees, and advisor fees.

Investment Fees

Every investment’s fee structure is unique, so it’s important to know that not all of the investments you pick will contain the same fees. Here are a few of the most common fees that we see within investments, specifically mutual funds:

Up Front Sales Loads: Basically, this is a fee that occurs at the point of purchase. Or in other words, on the upfront sale. Depending on the class of fund you pick, these can range from 3 – 8.5% of the price to purchase the investment. For example, if you have $100,000 that’s being invested in mutual fund XYZ, and it has a front-load sales charge of 5%, your upfront fee will be $5,000, which reduces your principal to $95,000. This means that day one after buying that investment you are fighting an uphill battle.

Back End Sales Load: These are the reverse of a front end load, meaning you will pay a percentage fee based on when you withdraw, and how much you withdraw.

Expense Ratio: This is the annual fee deducted from your account to pay the operating expenses of the fund you’ve chosen. These fees can range widely from 0.1%-3%, with 1% being the most common.

- The most expensive funds typically are actively managed which means they hire a fund manager to buy and sell securities in hopes of beating the market. The less expensive alternative are passively managed funds that track an index such as the S&P 500. The expense ratio in these funds can be as low as 0.1%.

Advisor Fees

Your advisor receives compensation in up to three different ways: they charge a fee for their advice, a fee for the money they manage, or they receive commissions from investments or insurance products they provide to you.

If your advisor is fee-based, they can either charge a flat fee for their advice, or they can charge an AUM (assets under management) fee as compensation for advising you in other areas. If they charge a flat fee for their advice, typically you will cut a check for every meeting with them and implement their advice on your own. The AUM fee structure can be a great option if you are looking for advice on a wide range of subjects and want your money managed without commission costs, and without having to do it yourself.

In some cases, advisors could charge an AUM fee on top of the sales load and internal expense ratio, which can dramatically increase your costs.

Every advisor’s fee structure is unique, and it’s critical to have your advisor clearly explain their fee structure.

Fees are necessary, but how much is too much?

Running an investment fund costs money. Record keeping, legal compliance, marketing, and many other services are required to maintain your investments, and the fees cover these expenses.

However, in general, the lower the fee, the better. Fees can have such a dramatic effect on your portfolio, that picking investments with lower fees typically produce better performance in the long run. If you find yourself paying 2 – 3% annually for investment and advisory fees, it may be time to ask your advisor what benefit you are receiving from those high fees. If the answer doesn’t meet your standards, then it could be time to start interviewing a new team.

How do I find my fees?

The first place to start is to ask your advisor about their fees. Get a clear understanding of what they are charging you, and what benefit you receive from it. If they are reluctant to share, that might be a warning sign.

Another place to look is the FINRA Fund Analyzer. It’s completely free, and it was created the Financial Industry Regulatory Authority (FINRA) to give investors transparency of fees before they invest. It’s important to know that using the FINRA Fund Analyzer alone could only give you half the picture of your fees. You might be missing your advisor fees they are charging on top of the fund fees you find in the Analyzer.

If you have a 401(k), there could be many fees that are hidden and it could take some digging to find them. We wrote an article that teaches you all about these 401(k) fees.

Bottom Line

Every compensation structure contains advantages and disadvantages. It is vital that you can understand your advisor’s fee structure and the investment fees they are recommending. Good advisors can communicate all aspects of their compensation and investment fees clearly.

If you want to arm yourself with some other questions to ask your advisor, check out the top 3 questions our clients have asked us in this article.

Continue Learning

Gain more Insights and empower your financial future with our articles and other resources.