When it comes to investing, how much risk should I take?

You may be familiar with risk tolerance, however using tolerance as the only measurement of risk may actually be a disservice to you. And worse, it could be jeopardizing your investments. So what should you do to understand how much risk to take? Let’s consider some other dimensions of measuring risk.

Let’s say you have a good friend who is starting a tech company. He approaches you and wonders if you’d like to be an investor. He is raising $3 million and is looking for a $50,000 minimum investment. You have been friends for a long time, you trust him, there is a significant opportunity that your investment will produce a high yield, and a significant probability that you will lose it all.

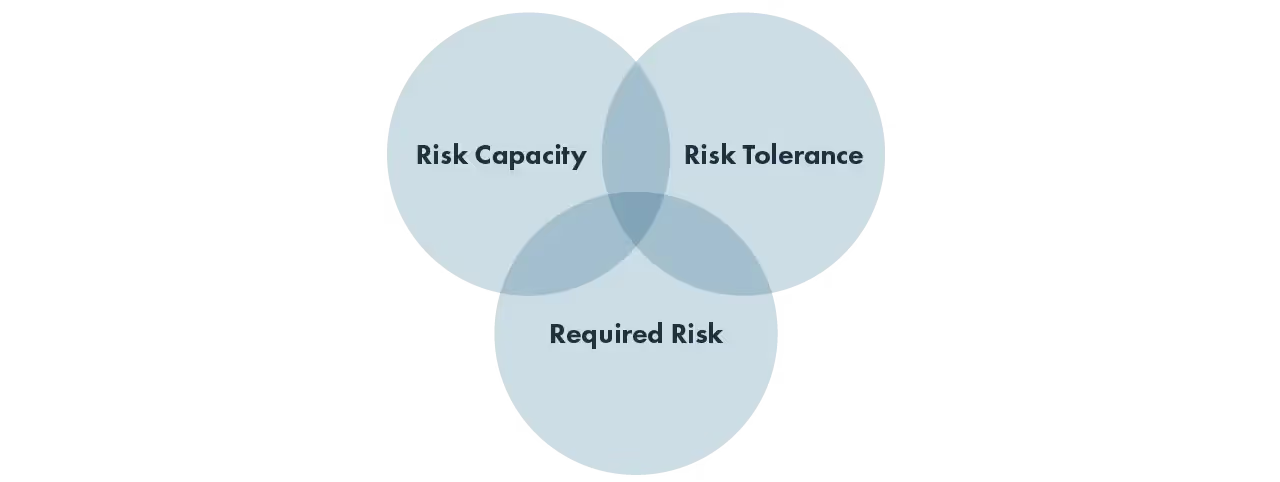

This is a high-risk investment. Can you afford to take this risk? Maybe. It depends on your specific financial situation. You could look at your ability to financially handle the loss and not have to change your lifestyle. This is your risk capacity. It measures how much you can suffer in loss and still be on track to hit your goals. Calculating your risk capacity involves the current risk in your assets, your asset levels, time horizon, and income objectives. If your annual income need in retirement is $60,000 and have guaranteed income sources like a pension, annuity, or social security that gives you $60,000 annually, your risk capacity is technically infinite. Any asset you have on top of your income sources can be “lost” and you will retire exactly how you’ve decided.

After you’ve figured out if you can afford to take the risk, the next step in measuring risk is finding out how much you must take to live the way you want. This is your required risk. Let’s say you have only $50,000 saved for retirement, but you need to have $2 million to retire the way you want, and you want to retire in three years. Let’s also say that if your friend’s company is successful, your investment will become $2 million in 3 years. In this situation, you most likely need to take the risk. This is an extreme example where the required risk far exceeds reality. If you need to take a huge risk and significantly increase your portfolio by investing in your friend’s company, realigning your goals might be necessary.

What’s your emotional response to this hypothetical investment opportunity? Are you worried about losing your money, or missing out on the potential gains? This is your risk tolerance. While your risk capacity and required risk are a measurable calculation, your risk tolerance is your own personal judgment.

Your risk tolerance, risk capacity, and required risk work together. Making a decision with just one dimension of risk could put you in a bad spot. For example, if your tolerance is high you may want to invest in your friend’s company. However, doing so could create a huge set back in your future if your risk capacity and risk required are low.

Understanding the full elements of risk will help you achieve your objectives, and help you understand exactly how much risk you can take. Knowing your risk tolerance is crucial, but without calculating your risk requirement and your risk capacity, you could end up making the wrong choice for your portfolio.

Here are a few questions to get you going:

- What is your desired income in retirement?

- What is your lifestyle cost and how long can you experience a negative market downturn before you have to change your lifestyle?

- How much can you stand to lose before your emotions take over your decisions?

Exposing your portfolio to the right risk for you is vital to retire the way you want. If you feel confident in your understanding of your tolerance and are wondering about the most effective way to calculate your risk capacity and risk tolerance, consider talking with a financial professional. Have them explain in detail how these risks can be calculated so that you can achieve your objectives.

Continue Learning

Gain more Insights and empower your financial future with our articles and other resources.